Impact of America Rescue Plan on Mortgage Servicing operations

Impact of America Rescue Plan on Mortgage Servicing operations

COVID-19 had an unprecedented impact on housing affordability for homeowners & renters alike. In order to keep the economy afloat - Coronavirus Aid, Relief, and Economic Security Act (CARES Act) was brought into effect. One of the key provisions of CARES Act was a - 12 months forbearance period to borrowers of federally backed loans. This provided much needed mortgage relief to homeowners albeit at a higher risk of default.

As the mortgage relief period headed to a close in March 2021, President Joe Biden announced the America Rescue Plan early this year to continue this beyond March. The plan not only allocates $1.9 trillion towards various state assistance programs but also extends the COVID-19 foreclosure & forbearance protection for homeowners.

Soon after this announcement, the Federal Housing Finance Agency (FHFA) extended the forbearance period for Fannie Mae and Freddie Mac loans to up to 18 months.

Undoubtedly, such foreclosure & forbearance relief extensions go a long way in protecting the homeowners during these difficult times. However, such measures also bring significant operational challenges for mortgage servicers & demand immediate action.

We have identified three key challenges that mortgage servicers are expected to face under the forbearance moratorium extension regime.

Massive Influx of customer enquiries

The America Rescue plan extends the forbearance enrollment window through June 2021, for borrowers who request for it. This means the volume of incoming customer inquiries & service call volumes are expected to climb up sharply in the coming weeks.

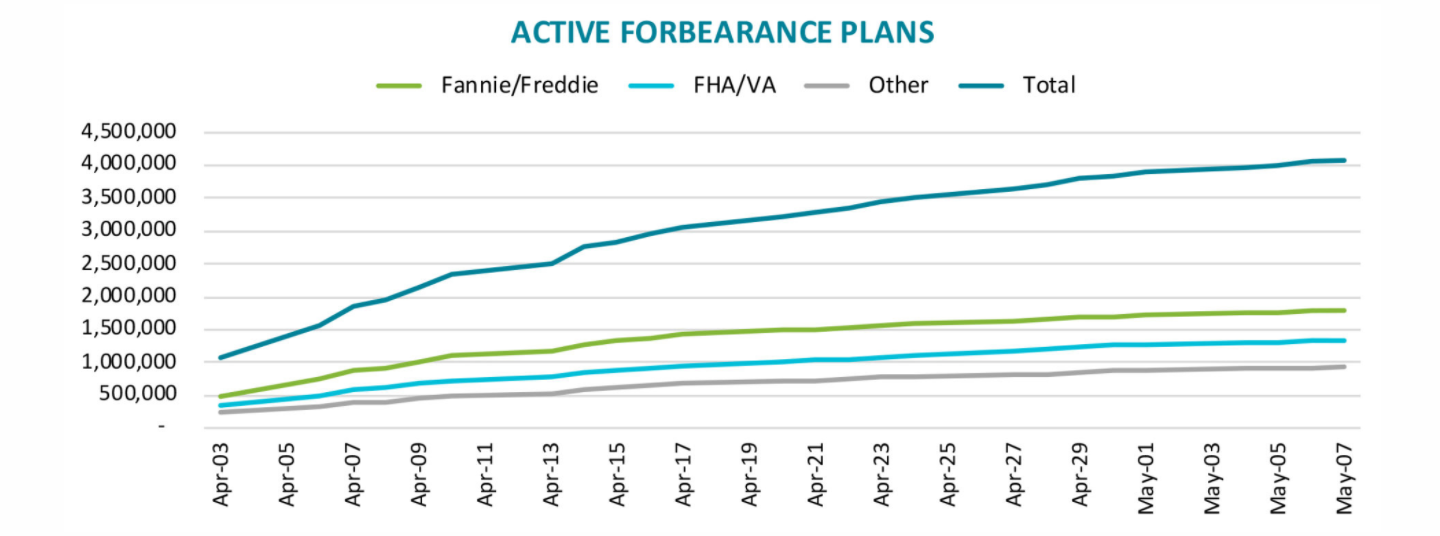

If we are to take any cue from the past, then we can expect the loan volumes to rise sharply in a short period of time. The below graph shows how the number of loans in active forbearance in 2020 increased by 300% in just 3 months, from 3rd April 2020 till 3rd May 2020.

As per Mortgage Bankers Association's (MBA) latest Forbearance and Call Volume Survey - the number of loans in forbearance has reduced to 5.14% of servicer’s portfolio volume. However, with the extension of the forbearance enrollment window, we may expect this number to go up in the first quarter of FY 2021-22.

Interestingly, MBA’s Forbearance & Call Volume survey also corroborates with this expected trend. One of the key findings was, for the week Mar 1- Mar 7, weekly servicer call center volume as a percent of servicing portfolio volume increased from 8.7% to 10%. This is the highest since the week ending April 19, 2020.

If this upward trend of customer call volumes continues, then it is likely to put excessive pressure on the customer service team and stretch the bandwidth of remote workforce on the side of mortgage servicers.

Operational challenges from reporting requirements

In May 2020, FHFA announced that Fannie Mae & Freddie Mac would allow payment deferral as the new repayment option for homeowners. This means borrowers can defer their missed mortgage payments until the home is sold, refinanced or paid off.

Further, according to the official whitehouse press release, foreclosure & forbearance extension plan under America Rescue plan provides for:

A. Extension of mortgage payment forbearance enrollment window till June 2021

B. Upto six months of additional mortgage payment forbearance for borrowers who entered forbearance on or before June 2020

As Fannie Mae & Freddie Mac comprise 53% of active loans - any increase in these loans entering the forbearance period under America Rescue plan will further compound the reporting challenges for mortgage servicers.

Let us understand this.

With deferral plans, servicers need to provide a consolidated statement to the investor. This statement should be presented as a sum of borrower’s missed payments including principal, interest and escrow - not as a breakdown.

This is in stark contrast to IRS reporting requirements. IRS will want to know the principal and interest components separately. Servicers will need to work closely with their IT department or technology vendor to track & retrieve this information, as some loans may be in the system for more than 20 years.

Loan Restructuring Challenges in compliance with State mortgage relief programs

America Rescue Plan offers forbearance extension support only to those borrowers of federally guaranteed loans, who request for it. If an extension is not requested, then servicers will have to work out a suitable loan restructuring program in compliance with state specific mortgage relief options. The same holds true for non-federally guaranteed loans, where forbearance extension is unavailable but the borrower is interested in opting for mortgage relief .

In other words, servicers need to be fully apprised of the latest state specific mortgage relief plan and compliance requirements – on top of the various loss mitigation plans already in place.

Robust technology that evaluates borrowers for loss mitigation options regardless of the investor, insurer, loan type, policy or program is critical during this time. The technology will also need to facilitate quick decisioning, while helping servicers remain compliant.

Conclusion

As the uncertainty and difficulties related to COVID-19 continue, servicers need to augment their operational capabilities to navigate through these challenges. This means, servicers must put in place an omni channel customer communication strategy to reduce the burden on call center infrastructure.

Simultaneously, servicers need to work closely with their technology MSPs to improve the responsiveness of their existing systems. This would allow them to streamline their loan restructuring operations in accordance to federal & state laws, while ensuring reporting compliance.

Such a holistic approach will not only ensure that mortgage servicers stay operationally robust but also offer a high standard of service to its borrowers during these difficult times of COVID-19.

Comments

Post a Comment